Workers compensation insurance ny cost – Workers’ compensation insurance ny cost is a crucial aspect for businesses in New York. Understanding the factors that influence its cost can help businesses optimize their insurance plans and protect their employees.

This guide will delve into the intricacies of workers’ compensation insurance in New York, exploring the insurance carriers, key factors affecting cost, coverage options, cost-saving strategies, legal considerations, and valuable resources available to businesses.

Insurance Carriers in New York

Several insurance carriers offer workers’ compensation insurance in New York. The top carriers include:

- The State Insurance Fund

- Zurich

- Travelers

- Hartford

- Liberty Mutual

The cost of workers’ compensation insurance in New York is determined by several factors, including:

- The size of the business

- The industry in which the business operates

- The number of employees

- The claims history of the business

Factors Affecting Cost

The cost of workers’ compensation insurance in New York is influenced by a number of factors, including the following:

Industry

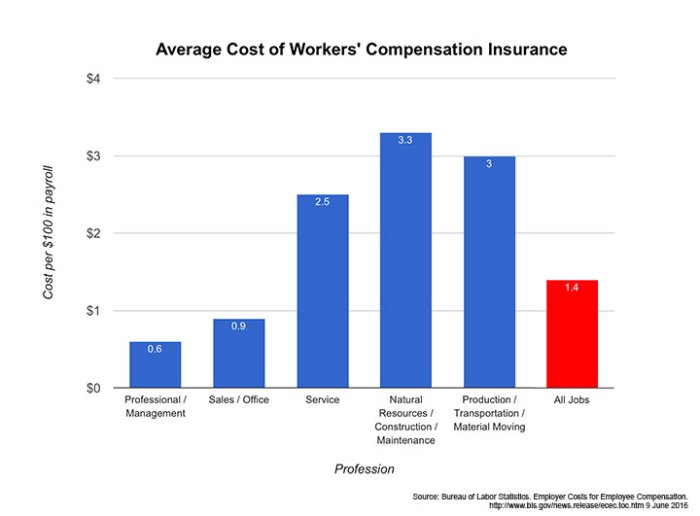

The industry in which a business operates can have a significant impact on the cost of workers’ compensation insurance. Businesses in high-risk industries, such as construction and manufacturing, typically pay higher premiums than businesses in low-risk industries, such as office work and retail.

Payroll

The size of a business’s payroll is another important factor that affects the cost of workers’ compensation insurance. The higher the payroll, the higher the premium. This is because the payroll is used to calculate the amount of benefits that the insurer will have to pay out in the event of a workplace injury or illness.

Workers’ compensation insurance in New York can be pricey, but it’s essential for protecting your business. If you’re looking for more affordable medical insurance options, consider exploring medical insurance in South Carolina. South Carolina has lower healthcare costs than New York, and you may be able to find a plan that meets your needs at a more affordable price.

However, it’s important to compare policies carefully before making a decision, as coverage and costs can vary widely.

Claims History

A business’s claims history can also affect the cost of workers’ compensation insurance. Businesses with a history of frequent or severe claims will typically pay higher premiums than businesses with a clean claims history. This is because the insurer will view these businesses as being more likely to file claims in the future.

Workers compensation insurance in New York can be a significant expense for businesses. The cost of coverage varies depending on the number of employees, the type of work they perform, and the company’s claims history. If you’re looking for ways to save money on your workers’ compensation insurance, you may want to consider asking your employees if they have vision insurance.

Many vision insurance plans cover LASIK surgery, which can help reduce the risk of workplace accidents and injuries. Is LASIK covered by insurance Cigna ? To find out, you can check your policy or contact your insurance provider. If you don’t have vision insurance, you may want to consider getting a policy.

It could save you money on your workers’ compensation insurance costs in the long run.

Experience Modification Factor (EMR)

The experience modification factor (EMR) is a rating factor that is used by insurers to adjust the cost of workers’ compensation insurance based on a business’s claims history. An EMR of 1.0 means that the business has an average claims history.

In New York, the cost of workers’ compensation insurance can vary widely depending on the industry, size of the business, and other factors. However, there are some things that all businesses can do to reduce their costs, such as implementing a strong safety program and partnering with a reputable insurance provider.

If you’re looking for a more affordable option, you may want to consider short term insurance plans illinois. These plans are designed to provide temporary coverage for employees who are not eligible for traditional workers’ compensation insurance. While they may not offer the same level of coverage, they can be a cost-effective way to protect your business.

An EMR of less than 1.0 means that the business has a better-than-average claims history, and an EMR of greater than 1.0 means that the business has a worse-than-average claims history.

Deductible

The deductible is the amount of money that a business must pay out of pocket before the insurer will begin to pay benefits. A higher deductible will result in a lower premium, and a lower deductible will result in a higher premium.

Coverage Options: Workers Compensation Insurance Ny Cost

Workers’ compensation insurance in New York offers a range of coverage options that tailor to the specific needs of businesses. The choice of coverage options significantly impacts the cost of insurance, as it determines the extent of protection provided and the level of risk assumed by the insurance carrier.

The cost of workers compensation insurance in New York can vary depending on a number of factors. For example, businesses in high-risk industries will typically pay more for coverage than businesses in low-risk industries. Additionally, businesses with a history of workplace accidents or injuries will also pay more for coverage.

If you are looking for more information on workers compensation insurance, you can check out san fernando valley heart insurance. They can provide you with a free quote and help you find the right coverage for your business. Ultimately, the cost of workers compensation insurance is a small price to pay for the peace of mind that comes with knowing that your employees are protected in the event of a workplace accident or injury.

Coverage options typically include:

Statutory Coverage

- Required by law and provides basic benefits to employees who suffer work-related injuries or illnesses.

- Covers medical expenses, lost wages, and disability benefits.

Employer’s Liability Coverage

- Provides additional protection to employers against lawsuits filed by employees alleging negligence or wrongdoing.

- Covers damages beyond those covered by statutory coverage, such as pain and suffering.

Voluntary Coverage

- Offers optional coverage that extends beyond statutory requirements.

- May include benefits such as vocational rehabilitation, death benefits, and coverage for occupational diseases.

Choice of Coverage Impacts Cost

The choice of coverage options directly affects the cost of workers’ compensation insurance. Higher levels of coverage provide more comprehensive protection but also increase the premiums. Businesses must carefully consider their specific risks and financial capabilities when selecting coverage options to ensure adequate protection without overpaying for unnecessary coverage.

Cost-Saving Strategies

Businesses in New York can implement a range of strategies to reduce the cost of workers’ compensation insurance. These strategies involve controlling risk factors, improving workplace safety, and optimizing insurance coverage.

Successful cost-saving measures include implementing safety training programs, establishing a return-to-work program, and negotiating favorable insurance rates.

Risk Control

Controlling risk factors is crucial for reducing workers’ compensation costs. Businesses can:

- Identify and mitigate workplace hazards

- Provide comprehensive safety training to employees

- Implement ergonomic measures to prevent injuries

- Maintain a clean and well-organized work environment

Workplace Safety

Improving workplace safety reduces the frequency and severity of accidents, lowering insurance costs. Businesses can:

- Establish a safety committee to identify and address safety concerns

- Encourage employee participation in safety programs

- Regularly inspect equipment and facilities for potential hazards

- Develop emergency response plans

Insurance Coverage Optimization

Optimizing insurance coverage ensures businesses have the right amount of coverage at the most affordable cost. Businesses can:

- Review their policy annually to ensure it meets their needs

- Consider increasing their deductible to lower premiums

- Negotiate favorable rates with insurance carriers

- Explore group insurance programs to obtain discounts

Legal Considerations

In New York, workers’ compensation insurance is mandatory for all businesses with one or more employees. It provides financial protection to employees who suffer work-related injuries or illnesses, regardless of fault. Employers who fail to obtain workers’ compensation insurance may face severe consequences.

Consequences of Non-Compliance:

- Fines and penalties:Businesses without workers’ compensation insurance may be fined up to $10,000 per day, per employee.

- Civil lawsuits:Injured employees can file lawsuits against their employers for damages, including medical expenses, lost wages, and pain and suffering.

- Criminal charges:In some cases, employers who knowingly fail to obtain workers’ compensation insurance may face criminal charges.

Resources for Businesses

Navigating the complexities of workers’ compensation insurance in New York can be daunting. To assist businesses, various resources are available to provide guidance and support.

The following organizations offer valuable information, resources, and support to businesses seeking to understand and manage their workers’ compensation insurance needs in New York:

New York State Department of Financial Services (DFS), Workers compensation insurance ny cost

- Website: https://www.dfs.ny.gov/insurance/workers_compensation

- Phone: (212) 480-6100

- Email: [email protected]

New York Compensation Insurance Rating Board (NYCIRB)

- Website: https://www.nycirb.org/

- Phone: (212) 349-0070

- Email: [email protected]

National Council on Compensation Insurance (NCCI)

- Website: https://www.ncci.com/

- Phone: (904) 226-4000

- Email: [email protected]

Insurance Information Institute (III)

- Website: https://www.iii.org/

- Phone: (212) 346-5500

- Email: [email protected]

Closing Notes

In conclusion, workers’ compensation insurance ny cost is a multifaceted topic that requires careful consideration. By understanding the factors that influence cost, businesses can make informed decisions to protect their employees and maintain compliance. Utilizing cost-saving strategies and leveraging available resources can help businesses optimize their insurance plans and minimize financial burdens.

Essential FAQs

What are the key factors that affect workers’ compensation insurance costs in New York?

The key factors include payroll, industry classification, claims history, and loss experience.

What are the different coverage options available for workers’ compensation insurance in New York?

The coverage options include medical benefits, disability benefits, and death benefits.

What are some practical strategies to reduce the cost of workers’ compensation insurance in New York?

Strategies include implementing safety programs, reducing workplace hazards, and seeking discounts for good safety records.