Delving into the realm of small business LLC insurance costs, this article unveils the intricacies of protecting your enterprise. From understanding various insurance types to exploring cost-saving strategies, we’ll guide you through the insurance landscape tailored specifically for LLCs.

The complexities of insurance can often leave small businesses perplexed. However, with a comprehensive understanding of the factors influencing insurance premiums and the diverse coverage options available, you can make informed decisions to safeguard your business.

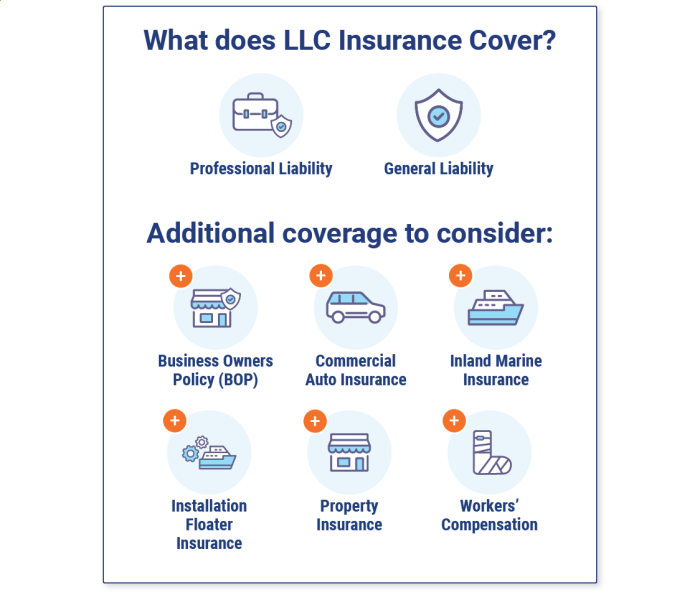

Types of Insurance for Small Businesses

Protecting your small business from unexpected events and liabilities is crucial for its success. Various types of insurance coverage are available to safeguard your company against financial losses and legal claims.

General Liability Insurance

General liability insurance provides coverage for bodily injury or property damage caused by your business operations or products. It protects you against lawsuits arising from accidents, injuries, or negligence on your premises or during business activities.

Example:A customer slips and falls in your store, resulting in a broken arm. General liability insurance would cover the medical expenses and legal costs associated with the accident.

Property Insurance

Property insurance covers physical assets owned or leased by your business, such as buildings, equipment, inventory, and furniture. It protects against damage or loss caused by events like fire, theft, vandalism, or natural disasters.

Example:A fire breaks out in your office, destroying equipment and inventory. Property insurance would cover the replacement or repair costs.

Professional Liability Insurance

Professional liability insurance, also known as errors and omissions (E&O) insurance, protects professionals who provide services or advice from claims of negligence or errors in their work. It covers financial losses and legal costs incurred due to mistakes or omissions in the services provided.

Example:An accountant makes an error in preparing a client’s tax return, resulting in financial losses for the client. Professional liability insurance would cover the costs of defending the lawsuit and any damages awarded.

Factors Affecting LLC Insurance Costs: Small Business Llc Insurance Cost

The cost of LLC insurance is influenced by several key factors, including industry, location, number of employees, and coverage limits.

The cost of insurance for a small business LLC can vary widely depending on a number of factors, such as the type of business, the number of employees, and the location of the business. To get an accurate quote, it’s important to compare quotes from multiple insurance companies.

For example, Does RV Insurance Cover Leaks A Comprehensive Guide provides a comprehensive guide to RV insurance coverage, including information on whether or not leaks are covered. By doing your research and comparing quotes, you can find the best possible insurance coverage for your small business LLC at an affordable price.

The type of industry in which an LLC operates can have a significant impact on insurance costs. For example, businesses in high-risk industries, such as construction or manufacturing, typically pay higher premiums than those in low-risk industries, such as office work or retail.

The location of an LLC can also affect insurance costs. Businesses located in areas with high crime rates or natural disasters tend to pay higher premiums than those in safer areas.

For small business owners, understanding insurance costs is crucial. Liability insurance, property insurance, and even specialized insurance like bobtail insurance are essential for protecting your business. For a comprehensive guide on bobtail insurance costs, check out How Much is Bobtail Insurance A Comprehensive Guide.

This guide provides insights into factors that influence bobtail insurance costs, helping you make informed decisions about your business’s insurance coverage.

The number of employees an LLC has can also impact insurance costs. Businesses with more employees are typically required to pay higher premiums than those with fewer employees.

Finally, the coverage limits chosen by an LLC can also affect insurance costs. Businesses that choose higher coverage limits typically pay higher premiums than those that choose lower coverage limits.

Coverage Limits

The coverage limits chosen by an LLC can have a significant impact on insurance costs. Higher coverage limits provide more protection for businesses, but they also come with higher premiums.

Small business owners should know that LLC insurance costs vary based on factors like location and coverage needs. However, if you need bobtail insurance, you can refer to How Much is Bobtail Insurance A Comprehensive Guide to learn more about its costs.

Small business owners should also note that the cost of bobtail insurance can also be affected by factors like the type of vehicle being insured and the driver’s experience.

When choosing coverage limits, businesses should consider the following factors:

- The value of their assets

- The potential for lawsuits

- The financial stability of the business

By carefully considering these factors, businesses can choose coverage limits that provide adequate protection without breaking the bank.

Cost Comparison for Different LLC Structures

The cost of insurance for an LLC can vary depending on the structure of the business. Single-member LLCs, which have only one owner, typically have lower insurance costs than multi-member LLCs, which have multiple owners. S corporations, which are a type of LLC that is taxed as a corporation, may also have different insurance costs than traditional LLCs.

Factors Affecting Costs

The following factors can affect the cost of insurance for an LLC:

- The type of business

- The number of employees

- The location of the business

- The amount of coverage desired

Cost Comparison Table

The following table compares the average cost of insurance for different LLC structures:

| LLC Structure | Average Annual Premium |

|---|---|

| Single-member LLC | $500-$1,000 |

| Multi-member LLC | $1,000-$2,000 |

| S corporation | $1,500-$2,500 |

Strategies for Reducing Insurance Costs

Small businesses can implement various strategies to reduce their insurance costs. These strategies aim to minimize risk, improve safety, and enhance insurability, resulting in lower premiums.

By understanding these strategies and implementing them effectively, small business owners can save money on their insurance policies while ensuring adequate protection for their businesses.

Increasing Deductibles

Increasing the deductible on insurance policies means agreeing to pay a higher out-of-pocket amount before the insurance coverage kicks in. This can significantly reduce premiums, as insurance companies view higher deductibles as a sign of lower risk.

For example, if a business raises its property insurance deductible from $500 to $1,000, it could save around 10-20% on the premium.

Implementing Safety Measures

Implementing safety measures in the workplace can reduce the likelihood of accidents, injuries, and property damage. This, in turn, can lead to lower insurance premiums.

Some examples of safety measures include:

- Installing security systems and alarms

- Providing safety training to employees

- Maintaining a clean and well-maintained workplace

- Conducting regular safety inspections

Obtaining Group Discounts

Small businesses can join industry associations or chambers of commerce to access group discounts on insurance policies. These discounts are negotiated by the organization on behalf of its members and can result in significant savings.

For example, a small business that joins a local chamber of commerce may be eligible for a 10% discount on its business insurance.

Insurance Coverage for Specific Industries

Insurance needs vary widely depending on the industry in which a business operates. Healthcare, construction, and retail businesses, for instance, have unique insurance requirements.Understanding the specific types of coverage essential for businesses in each industry is crucial for ensuring adequate protection.

This section explores the insurance needs of different industries, providing guidance on the essential types of coverage.

Healthcare Industry

The healthcare industry faces unique risks, including medical malpractice, patient privacy breaches, and regulatory compliance issues. Essential insurance coverage for healthcare businesses includes:

- Medical Malpractice Insurance: Protects against claims of negligence or errors in medical treatment.

- Professional Liability Insurance: Covers claims of errors or omissions in professional services, such as billing or record-keeping.

- Cyber Liability Insurance: Protects against data breaches and cyberattacks, safeguarding patient information.

- Employment Practices Liability Insurance: Covers claims related to discrimination, harassment, or wrongful termination.

Obtaining Quotes and Comparing Insurance Providers

Obtaining multiple insurance quotes is crucial for small businesses to ensure they secure the most suitable and cost-effective coverage. The process involves reaching out to different insurance providers and requesting a quote based on the business’s specific needs and risk profile.

Tips for Obtaining Quotes

- Provide accurate information:Disclose all relevant details about the business, its operations, and potential risks to ensure accurate quotes.

- Shop around:Contact multiple insurance providers to compare quotes and coverage options.

- Review the policy details:Carefully examine the terms, conditions, exclusions, and limits of each policy to ensure it aligns with the business’s needs.

Tips for Comparing Quotes

- Coverage:Ensure the policies provide adequate coverage for the identified risks and exposures.

- Cost:Compare the premiums and deductibles of different policies to determine the most cost-effective option.

- Reputation:Consider the reputation and financial stability of the insurance providers.

- Customer service:Evaluate the level of support and responsiveness offered by the insurance providers.

By following these tips, small businesses can obtain and compare insurance quotes effectively, enabling them to select the most appropriate policy that meets their specific needs and budget constraints.

Insurance for Home-Based Businesses

Home-based businesses face unique insurance considerations due to the overlap between personal and business activities. Understanding the limitations of homeowners insurance and the need for additional coverage is crucial.

Homeowners insurance generally covers the structure of the home, personal belongings, and liability for accidents that occur on the property. However, business activities may not be adequately covered under this policy.

Business Property and Liability Coverage

Additional insurance is typically required to cover business property, equipment, inventory, and liability associated with business operations. A business owner’s policy (BOP) is a comprehensive option that combines property and liability coverage specifically tailored to home-based businesses.

Insurance for Online Businesses

Online businesses face unique risks and liabilities that require specialized insurance coverage. Cyber liability insurance protects against data breaches, while business interruption insurance covers losses due to technology failures. E-commerce businesses may also need product liability insurance for claims related to defective products sold online.

Cyber Liability Insurance, Small business llc insurance cost

Cyber liability insurance covers financial losses and legal expenses resulting from data breaches, cyber attacks, and other online security incidents. It can help businesses protect sensitive customer information, comply with data privacy regulations, and mitigate the financial impact of cyber threats.

Data Breach Coverage

Data breach coverage is a specific type of cyber liability insurance that provides financial protection in the event of a data breach. It covers costs associated with notifying affected individuals, investigating the breach, and providing credit monitoring or identity theft protection services.

Understanding the costs of insurance for your small business LLC is crucial. If you’re curious about the insurance coverage and expenses for a specific vehicle, like the 2016 Acura MDX, check out 2016 Acura MDX Insurance The Ultimate Guide to Coverage and Cost.

This comprehensive guide provides valuable insights into insurance options and costs. Returning to the topic of small business LLC insurance, remember to carefully evaluate your coverage needs and compare quotes from different providers to secure the best protection at an affordable price.

Business Interruption Insurance

Business interruption insurance covers lost income and expenses if a business is forced to close temporarily due to a covered event, such as a technology failure or a cyber attack. This insurance can help businesses recover from the financial impact of technology-related disruptions.

E-commerce Product Liability Insurance

E-commerce businesses that sell products online may need product liability insurance to protect against claims related to defective products. This insurance covers legal expenses and damages awarded to customers who suffer injuries or property damage due to a defective product sold by the business.

Ultimate Conclusion

In conclusion, the cost of insurance for small business LLCs is a crucial consideration for business owners. By understanding the types of insurance, factors affecting costs, and strategies for reducing premiums, you can optimize your insurance coverage while minimizing expenses.

Remember, insurance is an investment in protecting your business, ensuring its resilience and long-term success.

FAQ Summary

What types of insurance are essential for small business LLCs?

General liability, property insurance, and professional liability insurance are fundamental coverage options for small business LLCs.

How can I reduce the cost of my LLC insurance?

Increasing deductibles, implementing safety measures, and obtaining group discounts are effective strategies for lowering insurance premiums.

What unique insurance needs do online businesses have?

Online businesses require specialized coverage such as cyber liability insurance and data breach coverage to mitigate risks associated with online operations.