As Michigan car insurance rates increase, it’s essential to understand the factors driving this surge and explore strategies to mitigate its impact. This comprehensive guide delves into the intricacies of Michigan’s insurance landscape, offering insights into the reasons behind rising premiums and practical tips for lowering your insurance costs.

From the influence of medical expenses to the impact of fraudulent claims, we’ll uncover the complexities of Michigan’s car insurance market. By comparing rates with neighboring states, we’ll gain a broader perspective on the factors shaping Michigan’s insurance landscape.

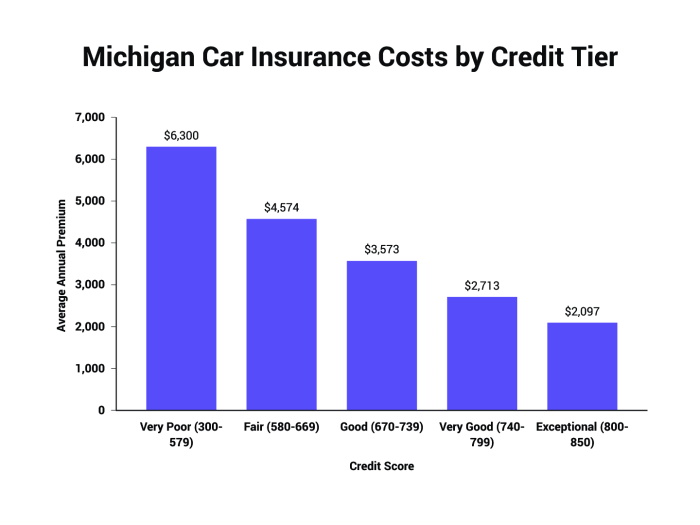

Factors Contributing to Michigan Car Insurance Rate Increases

Michigan car insurance rates have been on the rise in recent years, and there are a number of factors contributing to this trend.

One major factor is the rising cost of medical care. When people are injured in car accidents, their medical bills can be very expensive, and these costs are passed on to insurance companies in the form of higher premiums.

Michigan car insurance rates are on the rise, but you can still find affordable coverage if you shop around. If you’re a homeowner in Texas, you may also want to consider bundling your home and auto insurance to save even more money.

There are a number of great insurance companies in Texas, so be sure to do your research and compare quotes before you make a decision. You can find more information about the best home insurance companies in Texas here.

Michigan car insurance rates are expected to continue to rise in the coming years, so it’s important to start shopping around for affordable coverage now.

Increased Accident Rates and Fraudulent Claims

Another factor contributing to Michigan car insurance rate increases is the increase in accident rates. There are a number of reasons for this increase, including distracted driving, speeding, and drunk driving.

In addition to rising accident rates, fraudulent claims are also a problem in Michigan. These claims can drive up insurance costs for everyone, as insurance companies have to pay out more money to cover these fraudulent claims.

Natural Disasters and Weather Events

Finally, natural disasters and weather events can also contribute to Michigan car insurance rate increases. When these events occur, they can cause widespread damage to vehicles, which can lead to higher insurance claims and, ultimately, higher premiums.

Comparison of Michigan Car Insurance Rates with Other States

Michigan has consistently ranked among the states with the highest car insurance rates in the nation. To provide a clearer perspective, let’s compare Michigan’s rates with neighboring states.

Michigan car insurance rates have been on the rise lately, and it’s got me thinking about the big lou life insurance trophy wife. I mean, if you’re going to be paying more for car insurance, you might as well get some extra coverage for your spouse, right?

Just kidding! But seriously, it’s important to shop around for car insurance to get the best rate. Michigan car insurance rates can vary widely from company to company, so it’s worth taking the time to compare quotes.

Average Car Insurance Rates

| State | Average Annual Premium |

|---|---|

| Michigan | $2,699 |

| Ohio | $1,450 |

| Indiana | $1,580 |

| Illinois | $1,700 |

| Wisconsin | $1,850 |

As evident from the table, Michigan’s car insurance rates are significantly higher than those in neighboring states. Ohio, for instance, has rates that are nearly 46% lower than Michigan’s.

Factors Contributing to Rate Variations

The variations in car insurance rates among states can be attributed to several factors, including:

- Frequency of accidents:States with higher accident rates tend to have higher insurance premiums.

- Cost of medical care:Medical expenses associated with car accidents can vary significantly from state to state, impacting insurance costs.

- Fraud and litigation:States with higher levels of insurance fraud and lawsuits often have higher insurance rates.

- Government regulations:State laws and regulations regarding insurance coverage and claims can influence insurance rates.

Impact of Michigan’s No-Fault Insurance System

Michigan is the only state in the U.S. with a no-fault insurance system. This system differs significantly from traditional fault-based insurance systems and has a profound impact on car insurance rates in the state.

Under Michigan’s no-fault system, drivers are required to purchase personal injury protection (PIP) coverage, which provides benefits to the policyholder and their passengers regardless of who is at fault in an accident. This eliminates the need to determine fault, which can be a time-consuming and costly process.

Pros of No-Fault System, Michigan car insurance rates increase

- Reduced Litigation:By eliminating the need to determine fault, the no-fault system reduces the number of lawsuits filed after car accidents, which lowers legal costs for insurance companies and policyholders.

- Faster Claim Resolution:The no-fault system allows accident victims to receive benefits quickly, regardless of fault, which can help them cover medical expenses and lost wages.

- Lower Insurance Premiums:The reduced litigation and faster claim resolution result in lower administrative costs for insurance companies, which can translate into lower premiums for policyholders.

Cons of No-Fault System

- Higher PIP Premiums:While overall insurance premiums may be lower under the no-fault system, PIP coverage can be more expensive than traditional liability coverage.

- Limited Coverage:The no-fault system only provides coverage for medical expenses, lost wages, and other economic losses. It does not cover non-economic damages such as pain and suffering.

- Fraud Potential:The no-fault system can create an incentive for fraud, as individuals may be tempted to exaggerate their injuries or file fraudulent claims.

The impact of Michigan’s no-fault insurance system on car insurance rates is complex and depends on a variety of factors. While the system has some advantages, it also has some drawbacks. Ultimately, the decision of whether or not to maintain no-fault insurance in Michigan is a personal one that should be made after carefully considering the pros and cons.

Strategies for Lowering Car Insurance Rates in Michigan: Michigan Car Insurance Rates Increase

Michigan’s high car insurance rates can be a burden on drivers. However, there are several strategies that drivers can employ to lower their rates and save money.

Improving Driving Habits

One of the most effective ways to lower car insurance rates is to improve driving habits. This includes:

- Avoiding speeding and reckless driving

- Paying attention to the road and avoiding distractions

- Maintaining a clean driving record

Installing Safety Features

Installing safety features in vehicles can also help to lower car insurance rates. These features include:

- Anti-lock brakes

- Airbags

- Anti-theft devices

Increasing Deductibles and Bundling Policies

Increasing deductibles and bundling policies can also save money on car insurance. A deductible is the amount of money that the driver is responsible for paying out of pocket before the insurance company begins to cover the costs of a claim.

Michigan car insurance rates have been on the rise in recent years, making it more important than ever to find affordable coverage. One option to consider is navy federal term life insurance , which offers competitive rates and flexible coverage options.

By comparing quotes from multiple insurers, you can find the best deal on car insurance that meets your needs and budget. Don’t let rising insurance costs break the bank – explore your options and secure affordable coverage today.

By increasing the deductible, the driver can lower their insurance premium. Bundling policies, such as combining car and home insurance, can also save money.

Michigan car insurance rates are on the rise, and it’s important to make sure you have the coverage you need at a price you can afford. If you’re looking for a way to save money on car insurance, you may want to consider getting a quote from a company that offers utah state minimum car insurance.

These companies can often offer lower rates than traditional insurance companies, and they can still provide you with the coverage you need to protect yourself and your vehicle. Even if you don’t live in Utah, it’s worth getting a quote from a company that offers this type of insurance.

You may be surprised at how much you can save.

Discounts Available to Michigan Drivers

There are also a number of discounts available to Michigan drivers that can help to lower car insurance rates. These discounts include:

- Good driver discounts

- Multi-car discounts

- Senior citizen discounts

- Military discounts

Government Regulations and Industry Trends

Government regulations and industry trends play a significant role in shaping car insurance rates in Michigan. Recent legislative changes and emerging industry trends have a direct impact on the cost of coverage for Michigan drivers.

One notable legislative change in recent years was the passage of the Michigan Catastrophic Claims Association (MCCA) reform bill in 2019. This bill introduced a fee schedule for medical expenses related to auto accidents, resulting in a decrease in overall insurance costs for Michigan drivers.

However, the MCCA reform is currently facing legal challenges, and its long-term impact on rates remains uncertain.

Role of Insurance Regulators

Insurance regulators in Michigan have the responsibility of monitoring and controlling car insurance rates. The Michigan Department of Insurance and Financial Services (DIFS) has the authority to review and approve rate filings submitted by insurance companies. The DIFS also conducts market analysis and investigations to ensure that rates are fair and reasonable for consumers.

The DIFS has taken several steps to address the high cost of car insurance in Michigan. In 2020, the DIFS implemented a new rate review process that requires insurance companies to provide more detailed information to justify their rate filings.

The DIFS has also been working with insurance companies to develop new products and programs that make car insurance more affordable for Michigan drivers.

Emerging Industry Trends

Several emerging industry trends could further affect car insurance rates in Michigan. One trend is the increasing use of telematics devices. Telematics devices track driving behavior and can be used to reward safe drivers with discounts on their insurance premiums.

Another trend is the rise of usage-based insurance (UBI) programs. UBI programs charge drivers based on how much they drive and how safely they drive.

These trends have the potential to make car insurance more affordable for Michigan drivers, but they also raise concerns about privacy and data security. The DIFS is currently reviewing the use of telematics devices and UBI programs in Michigan to ensure that they are implemented fairly and in a way that protects consumer privacy.

Summary

Navigating the ever-changing world of car insurance can be daunting, but by staying informed and implementing smart strategies, you can minimize the financial burden of rising rates. Remember, driving safely, taking advantage of discounts, and bundling policies are just a few ways to keep your insurance costs under control.

Quick FAQs

Why are Michigan car insurance rates increasing?

Factors contributing to rising rates include increasing medical costs, higher accident rates, and fraudulent claims.

How does Michigan’s no-fault insurance system affect rates?

Michigan’s unique no-fault system provides certain benefits to accident victims but can also lead to higher insurance costs.

What strategies can I use to lower my car insurance rates in Michigan?

Improving driving habits, installing safety features, and bundling policies are effective ways to reduce your premiums.