Navigating the complexities of medical insurance plans for individuals can be daunting, but it doesn’t have to be. This comprehensive guide will break down the different types of plans, coverage, costs, and enrollment processes to empower you in making informed decisions about your healthcare.

From understanding the nuances of HMOs, PPOs, and EPOs to calculating premiums and maximizing benefits, this guide will equip you with the knowledge and tools you need to choose the right plan that meets your unique needs and budget.

Types of Medical Insurance Plans for Individuals

Medical insurance plans provide coverage for various healthcare expenses, and individuals can choose from different types of plans based on their needs and preferences.

The primary types of medical insurance plans for individuals include:

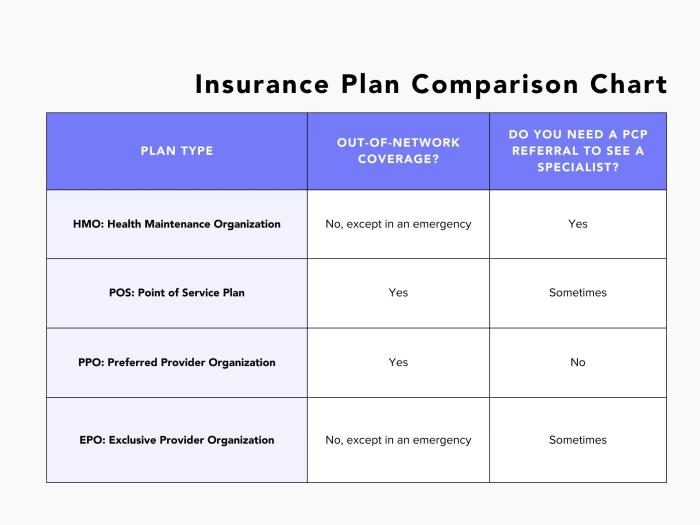

Health Maintenance Organizations (HMOs)

- Provide comprehensive coverage within a network of healthcare providers.

- Typically have lower premiums and out-of-pocket costs.

- Require referrals from a primary care physician for specialist visits.

- Example: Kaiser Permanente

Preferred Provider Organizations (PPOs)

- Offer more flexibility in choosing healthcare providers, both within and outside the network.

- Have higher premiums and out-of-pocket costs than HMOs.

- Do not require referrals for specialist visits.

- Example: Blue Cross Blue Shield

Exclusive Provider Organizations (EPOs)

- Similar to HMOs, but with a narrower network of healthcare providers.

- Typically have lower premiums than PPOs.

- Do not allow out-of-network coverage.

- Example: Aetna EPO

Coverage and Benefits of Medical Insurance Plans

Medical insurance plans for individuals provide a range of coverage and benefits to help cover the costs of medical care. These plans typically include coverage for a variety of services, including doctor visits, hospital stays, prescription drugs, and preventive care.

The specific coverage and benefits included in a medical insurance plan will vary depending on the type of plan and the insurance company. However, some of the most common coverage and benefits include:

Covered Services

Most medical insurance plans for individuals cover a wide range of services, including:

- Doctor visits

- Hospital stays

- Prescription drugs

- Preventive care

- Mental health care

- Substance abuse treatment

Deductibles

A deductible is the amount of money you have to pay out-of-pocket before your insurance coverage begins. Deductibles can vary depending on the type of plan and the insurance company. Some plans have a separate deductible for each type of service, such as a deductible for doctor visits and a deductible for hospital stays.

Understanding medical insurance plans for individuals can be a bit overwhelming. If you’re looking for more protection, consider getting a state farm liability insurance quote. It can provide peace of mind and financial protection in case of accidents or unexpected events.

Additionally, having a solid medical insurance plan ensures you have access to necessary healthcare services.

Copays

A copay is a fixed amount of money that you have to pay for each covered service. Copays can vary depending on the type of service and the insurance company. Some plans have a copay for each doctor visit, while others have a copay for each prescription drug.

Out-of-Pocket Maximums

An out-of-pocket maximum is the most you will have to pay out-of-pocket for covered services in a year. Out-of-pocket maximums can vary depending on the type of plan and the insurance company. Once you reach your out-of-pocket maximum, your insurance company will pay for 100% of the cost of covered services for the rest of the year.

Table Comparing the Coverage and Benefits of Different Types of Plans

The following table compares the coverage and benefits of different types of medical insurance plans for individuals:

| Type of Plan | Coverage | Deductible | Copay | Out-of-Pocket Maximum |

|---|---|---|---|---|

| Bronze | Basic coverage | High | Low | High |

| Silver | More comprehensive coverage | Moderate | Moderate | Moderate |

| Gold | Most comprehensive coverage | Low | High | Low |

| Platinum | Most comprehensive coverage with the lowest out-of-pocket costs | Very low | Very high | Very low |

Costs and Premiums of Medical Insurance Plans

The costs and premiums of medical insurance plans for individuals are determined by a variety of factors, including age, health status, location, and the type of plan selected. Premiums are typically higher for older individuals, those with pre-existing medical conditions, and those who live in areas with high healthcare costs.

Factors Affecting Premiums

The following factors can affect the premiums of medical insurance plans for individuals:

- Age:Premiums tend to increase with age, as older individuals are more likely to experience health problems.

- Health status:Individuals with pre-existing medical conditions or a history of health problems may be charged higher premiums.

- Location:Premiums can vary significantly depending on the location of the individual. Areas with high healthcare costs, such as large cities, typically have higher premiums.

- Type of plan:Premiums for different types of medical insurance plans can vary significantly. Plans with more comprehensive coverage, such as PPOs and EPOs, typically have higher premiums than plans with more limited coverage, such as HMOs.

Average Premiums

The average premiums for different types of medical insurance plans for individuals can vary significantly depending on the factors discussed above. According to the Kaiser Family Foundation, the average annual premium for employer-sponsored health insurance in 2021 was $22,221 for family coverage and $7,739 for individual coverage.

For individuals who purchase health insurance on the individual market, premiums can be higher. According to the Health Insurance Marketplace, the average monthly premium for a benchmark Silver plan in 2023 is $456 for a 40-year-old non-smoker. However, premiums can vary significantly depending on the individual’s age, health status, location, and the type of plan selected.

Choosing the Right Medical Insurance Plan

Navigating the world of medical insurance can be overwhelming. To make an informed decision, it’s crucial to understand your needs and compare different plans thoroughly.

Consider Your Coverage Needs

- Determine the types of medical services you’re likely to use, such as doctor visits, hospital stays, or prescription drugs.

- Consider any pre-existing conditions or ongoing health concerns that may affect your coverage.

Assess Costs and Premiums, Medical insurance plans for individuals

- Calculate your budget for monthly premiums and potential out-of-pocket expenses, such as deductibles and copays.

- Compare plans based on their overall costs, including both premiums and deductibles.

Evaluate Provider Network

- Choose a plan that includes a network of healthcare providers that meet your needs.

- Consider the proximity of providers, their availability, and their reputation.

Compare Plans and Make an Informed Decision

Once you have considered your needs, costs, and provider network, it’s time to compare plans. Use online tools or consult with an insurance agent to review different options and make an informed decision that meets your specific requirements.

For individuals, medical insurance plans provide essential coverage for various health expenses. If you’re struggling with alcohol addiction, you may wonder, does insurance cover alcohol rehab ? Fortunately, many medical insurance plans offer coverage for alcohol rehabilitation programs, allowing you to access professional help and embark on the path to recovery.

Enrolling in a Medical Insurance Plan

Enrolling in a medical insurance plan for individuals is a crucial step in securing access to healthcare services. The process involves several key steps that must be followed carefully to ensure successful enrollment.

Open Enrollment Periods

Open enrollment periods are specific timeframes during which individuals can enroll in or change their medical insurance plans. These periods typically occur once a year, usually during the fall, and provide an opportunity for individuals to compare plans and make informed decisions.

Special Enrollment Periods

Special enrollment periods are exceptions to the open enrollment periods and allow individuals to enroll in a medical insurance plan outside of the regular timeframe. These periods are typically triggered by certain life events, such as losing health insurance coverage, getting married, or having a baby.

Completing an Application

To enroll in a medical insurance plan, individuals must complete an application form provided by the insurance company. The application typically requires personal information, health history, and financial details. It is essential to provide accurate and complete information on the application to ensure a smooth enrollment process.

Submitting the Application

Once the application is completed, it must be submitted to the insurance company. This can be done online, by mail, or in person at an insurance agent’s office. The insurance company will review the application and determine eligibility for coverage.

Finding the right medical insurance plan for individuals can be a daunting task, but it’s crucial to have adequate coverage. While you’re at it, you might also wonder if you need car insurance for doordash. Whether you’re a seasoned delivery driver or just starting out, understanding your insurance needs is essential.

Once you’ve sorted out your car insurance, don’t forget to revisit medical insurance plans for individuals to ensure you have the protection you need.

Using a Medical Insurance Plan

Understanding how to effectively utilize your medical insurance plan is crucial to maximizing its benefits and minimizing out-of-pocket expenses. This guide will provide you with the essential steps and tips to ensure you get the most out of your coverage.

Finding In-Network Providers

In-network providers are healthcare professionals who have contracted with your insurance company to provide services at negotiated rates. Using in-network providers can significantly reduce your out-of-pocket costs, as you will typically pay less for services compared to using out-of-network providers.

When exploring medical insurance plans for individuals, consider options like humana part d supplemental insurance. It provides additional coverage beyond basic plans, catering to specific healthcare needs. Understanding the various options available is crucial for selecting a plan that aligns with your individual requirements, ensuring comprehensive medical protection.

- Check your insurance company’s website or call their customer service line to find a list of in-network providers in your area.

- When scheduling an appointment, verify with the provider’s office that they are in-network with your insurance plan.

Filing Claims

When you receive medical services, you will typically need to file a claim with your insurance company to be reimbursed for covered expenses. Filing a claim involves submitting documentation, such as the bill from the healthcare provider and a completed claim form, to your insurance company.

- Most insurance companies offer online portals or mobile apps where you can submit claims electronically.

- You can also mail or fax your claim form and supporting documentation to your insurance company.

Appealing Denied Claims

If your insurance company denies a claim, you have the right to appeal the decision. The appeals process typically involves submitting additional documentation or providing a written explanation of why you believe the claim should be covered.

- Contact your insurance company to request an appeal form.

- Gather any relevant medical records or documentation to support your appeal.

Maximizing Benefits and Minimizing Out-of-Pocket Costs

There are several ways to maximize the benefits of your medical insurance plan and minimize your out-of-pocket costs:

- Use in-network providers whenever possible.

- Take advantage of preventive care services, such as annual checkups and screenings, which are typically covered at no cost.

- Ask your doctor about generic medications, which are often more affordable than brand-name medications.

- Consider using a health savings account (HSA) or flexible spending account (FSA) to set aside pre-tax dollars for healthcare expenses.

Concluding Remarks

Choosing the right medical insurance plan is a crucial step towards securing your health and financial well-being. By understanding the intricacies of coverage, costs, and enrollment, you can confidently navigate the healthcare system and ensure access to quality care when you need it most.

FAQ Guide

What is the difference between an HMO and a PPO?

An HMO (Health Maintenance Organization) typically offers lower premiums but requires you to stay within a network of providers. A PPO (Preferred Provider Organization) provides more flexibility in choosing providers but may come with higher premiums.

What is a deductible?

A deductible is the amount you pay out-of-pocket before your insurance starts covering expenses.

How can I lower my health insurance premiums?

Consider a plan with a higher deductible, opt for generic medications, and take advantage of wellness programs offered by your insurer.