Is life insurance for life? The answer is a resounding yes! In this article, we delve into the concept of life insurance for life, exploring its benefits, considerations, and how it differs from other life insurance options. Join us as we uncover the nuances of lifelong coverage and its impact on financial security and legacy planning.

Life insurance for life, also known as whole life insurance, provides lifelong coverage, ensuring financial protection for your loved ones throughout your entire life. It offers a unique combination of insurance coverage and cash value accumulation, making it a valuable tool for long-term financial planning and wealth building.

Overview of Life Insurance

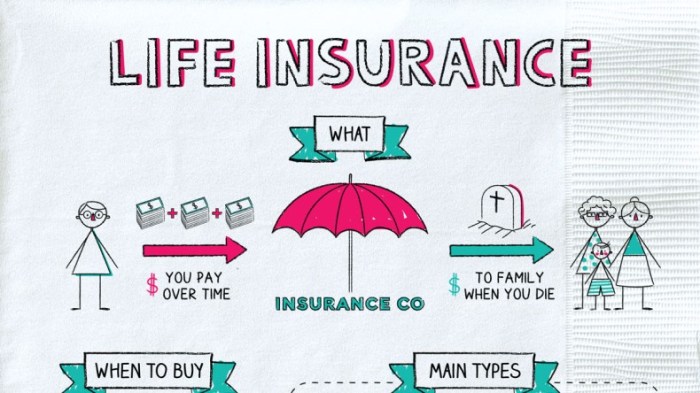

Life insurance is a contract between an insurance company and an individual, where the insurance company agrees to pay a sum of money to the individual’s beneficiaries upon their death in exchange for regular premium payments. The primary purpose of life insurance is to provide financial security and protection for loved ones in the event of the policyholder’s passing.

There are different types of life insurance policies available, each offering varying coverage options and benefits. The most common types include:

Term Life Insurance

Term life insurance provides coverage for a specific period, such as 10, 20, or 30 years. If the policyholder dies within the term, the beneficiaries receive the death benefit. Term life insurance premiums are typically lower than whole life insurance premiums, but the coverage expires at the end of the term unless the policy is renewed.

Whole Life Insurance

Whole life insurance provides coverage for the entire life of the policyholder, regardless of when they die. Whole life insurance premiums are higher than term life insurance premiums, but the policyholder also accumulates a cash value component that can be borrowed against or withdrawn.

Universal Life Insurance

Universal life insurance is a flexible type of life insurance that allows the policyholder to adjust the death benefit and premium payments over time. Universal life insurance policies also have a cash value component that can be accessed.

Variable Life Insurance

Variable life insurance is a type of life insurance that invests the cash value component in a variety of investment options, such as stocks and bonds. The death benefit and cash value of a variable life insurance policy fluctuate based on the performance of the investments.

Understanding the Term “For Life”

The phrase “life insurance for life” refers to insurance policies that provide coverage for the entire life of the insured individual, as long as the premiums are paid on time. Unlike term life insurance policies, which have a fixed coverage period, whole life insurance policies are designed to provide lifelong protection.

Whole Life Insurance Policies

Whole life insurance policies are permanent life insurance contracts that provide coverage for the entire life of the insured person. These policies typically have a cash value component that grows over time, providing a savings element in addition to the death benefit.

Cash Value Accumulation

The cash value component of a whole life insurance policy is an important feature that distinguishes it from term life insurance. This value accumulates over time, based on the policy’s premiums and investment returns. The cash value can be borrowed against or withdrawn by the policyholder, providing access to funds during the insured person’s lifetime.

Benefits of Life Insurance for Life: Is Life Insurance For Life

Life insurance for life provides financial security and peace of mind throughout an individual’s lifetime. It offers several benefits that make it a valuable financial planning tool.

Financial Security

Lifelong coverage ensures financial protection for loved ones in the event of the policyholder’s passing. The death benefit provides a lump sum payment that can be used to cover expenses such as funeral costs, outstanding debts, and mortgage payments. This financial cushion helps alleviate the financial burden on surviving family members and ensures their financial stability.

Peace of Mind, Is life insurance for life

Life insurance for life offers peace of mind knowing that loved ones will be financially secure in the future. It eliminates the uncertainty and worry associated with unexpected events. Policyholders can rest assured that their family’s financial needs will be met, regardless of when they pass away.

Legacy Planning

Whole life insurance can serve as a legacy planning tool. The cash value component grows over time, providing a tax-advantaged way to accumulate wealth. Policyholders can access this cash value through loans or withdrawals while they are alive, or it can be passed on to beneficiaries as part of their inheritance.

Examples of Benefits

- Ensuring financial stability for surviving spouses and children by covering expenses and debts.

- Providing funds for education, healthcare, or other future expenses for loved ones.

- Creating a tax-free legacy for beneficiaries through the cash value component.

Considerations for Life Insurance for Life

Choosing a whole life insurance policy is a significant financial decision that requires careful consideration. Factors such as affordability, long-term financial planning, and individual needs and circumstances should be thoroughly evaluated to make an informed choice.

Affordability

Affordability is crucial when selecting a life insurance policy. Premiums should fit comfortably within your budget without straining your finances. Consider your current income, future earning potential, and other financial obligations to determine a premium amount that you can consistently pay over the long term.

Long-Term Financial Planning

Life insurance for life is a long-term commitment. It is essential to consider your financial goals and objectives over the entire policy term. The policy should align with your long-term financial plan, ensuring that it does not interfere with other important financial priorities, such as retirement savings or education funding.

Individual Needs and Circumstances

Individual needs and circumstances vary greatly. Consider your family situation, income level, health status, and risk tolerance when selecting a policy. The amount of coverage, policy type, and premium payment options should be tailored to your specific needs and circumstances.

Comparison to Other Life Insurance Options

Whole life insurance, term life insurance, and universal life insurance are the three main types of life insurance policies. Each type has its own advantages and disadvantages, and the best option for you will depend on your individual needs and circumstances.

Whole Life Insurance

- Provides coverage for your entire life, as long as you continue to pay the premiums.

- Premiums are typically higher than term life insurance, but they are fixed and will not increase over time.

- Builds cash value over time, which can be borrowed against or withdrawn.

Term Life Insurance

- Provides coverage for a specific period of time, such as 10, 20, or 30 years.

- Premiums are typically lower than whole life insurance, but they will increase as you get older.

- Does not build cash value.

Universal Life Insurance

- Provides coverage for your entire life, as long as you continue to pay the premiums.

- Premiums are flexible and can be adjusted up or down as needed.

- Builds cash value over time, which can be borrowed against or withdrawn.

The following table summarizes the key differences between whole life insurance, term life insurance, and universal life insurance:

| Feature | Whole Life Insurance | Term Life Insurance | Universal Life Insurance |

|---|---|---|---|

| Coverage | Entire life | Specific period of time | Entire life |

| Premiums | Fixed and higher | Lower but increase with age | Flexible |

| Cash value | Builds over time | Does not build | Builds over time |

Last Recap

In conclusion, life insurance for life is a powerful financial tool that provides peace of mind, financial security, and a lasting legacy for your loved ones. By understanding the concept of lifelong coverage, its benefits, and considerations, you can make informed decisions about your life insurance needs and ensure the well-being of your family for generations to come.

Helpful Answers

Is life insurance for life really for life?

Yes, whole life insurance policies provide coverage for your entire life, as long as the premiums are paid.

What is the difference between whole life insurance and term life insurance?

Whole life insurance provides lifelong coverage and cash value accumulation, while term life insurance provides coverage for a specific period, such as 10, 20, or 30 years.

How does cash value accumulation work in whole life insurance?

A portion of your premiums goes towards a cash value account, which grows over time on a tax-deferred basis. You can borrow against or withdraw from the cash value, but doing so may affect the death benefit.