Dive into the fascinating world of insurance rates by zip code, where your address holds the key to understanding the financial implications of your coverage. From understanding the factors that influence these variations to exploring the impact on consumers and the insurance industry, this comprehensive guide will unravel the complexities of this intricate system.

Insurance Rates by Zip Code

Insurance rates vary depending on your zip code. This is because insurance companies use a variety of factors to determine your risk, and one of those factors is your location.

For example, if you live in an area with a high crime rate, you may be more likely to file a claim, which can lead to higher insurance rates. Similarly, if you live in an area that is prone to natural disasters, such as hurricanes or earthquakes, you may also be more likely to file a claim, which can lead to higher insurance rates.

Factors that Contribute to Variations

There are a number of factors that contribute to variations in insurance rates by zip code. These factors include:

- Crime rate

- Natural disaster risk

- Population density

- Property values

- Age of homes

- Construction type

Data Analysis

Data analysis plays a crucial role in understanding the complexities of insurance rates by zip code. By gathering data from various sources, we can gain valuable insights into the factors influencing insurance premiums and identify patterns that can help us make informed decisions.

To conduct a comprehensive analysis, we first need to collect data from multiple sources. This may include insurance companies, government agencies, and industry research firms. The data should include information on insurance rates, zip codes, and other relevant factors such as property values, crime rates, and population density.

Data Organization and Presentation

Once the data is gathered, it needs to be organized and presented in a clear and concise format. A well-structured table is an effective way to present the data, allowing for easy comparison and identification of trends. The table should include columns for zip code, insurance rate, and other relevant factors.

Data Analysis

With the data organized, we can begin analyzing it to identify trends and patterns. Statistical techniques, such as regression analysis and correlation analysis, can be used to determine the relationship between insurance rates and various factors. By examining the data, we can identify areas with higher or lower insurance rates and explore the underlying causes.

For example, we may find that insurance rates are higher in zip codes with higher crime rates or lower property values. This information can be valuable for insurance companies in setting rates and for consumers in making informed decisions about their insurance coverage.

Impact on Consumers

Insurance rates by zip code can have a significant impact on consumers. Consumers in areas with higher rates may have to pay more for the same coverage than those in areas with lower rates. This can be a financial burden for consumers, especially those who are already struggling to make ends meet.

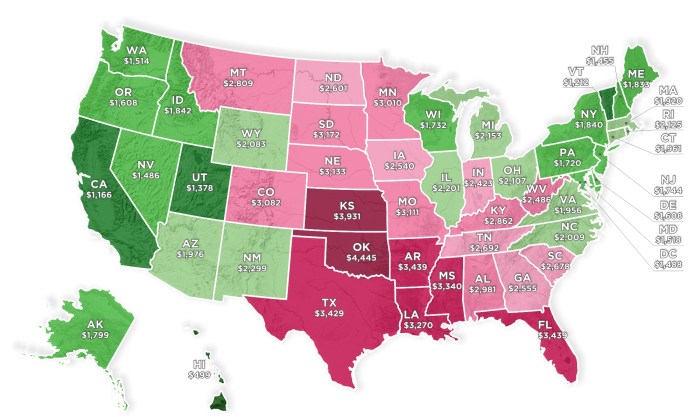

For example, a study by the National Association of Insurance Commissioners (NAIC) found that auto insurance rates can vary by as much as 100% from one zip code to another. This means that a driver in one zip code could pay twice as much for the same coverage as a driver in another zip code.

Financial Impact

The financial impact of higher insurance rates can be significant. For example, a consumer who pays $1,000 per year for auto insurance could end up paying $2,000 per year if they move to a zip code with higher rates. This could be a major financial burden for a consumer who is already struggling to make ends meet.

Consequences of Higher or Lower Rates

Higher insurance rates can also have a number of other consequences for consumers. For example, consumers may be forced to reduce their coverage or even drop their insurance altogether. This can leave them financially vulnerable in the event of an accident or other covered event.

On the other hand, lower insurance rates can make it easier for consumers to afford the coverage they need. This can give them peace of mind and financial security.

Insurance Industry Practices: Insurance Rates By Zip Code

Insurance companies heavily rely on zip codes as a factor in determining insurance rates. This practice has significant implications for consumers, raising ethical concerns and potential biases or discrimination.

Use of Zip Codes in Rate Determination

Insurance companies use zip codes to assess the risk associated with insuring a particular location. They collect data on factors such as crime rates, property values, and natural disaster risks within each zip code. This data is then used to calculate insurance rates for that area.

Ethical Implications

The use of zip codes in rate determination raises ethical concerns because it can lead to unfair or discriminatory practices. For example, if a zip code has a high crime rate, all residents within that zip code may be charged higher insurance rates, even if they have a good driving record or have taken steps to secure their property.

Potential Biases and Discrimination, Insurance rates by zip code

The use of zip codes in rate determination can also perpetuate biases and discrimination. For example, if a zip code is predominantly populated by a particular racial or ethnic group, the insurance rates in that zip code may be higher due to factors such as higher crime rates or lower property values.

This can lead to systemic discrimination, where certain groups of people are unfairly burdened with higher insurance costs.

Regulation and Policy

Insurance rates by zip code are subject to various regulations and policies aimed at ensuring fairness, transparency, and consumer protection. These regulations vary by state and may include:

State Insurance Laws:Most states have insurance laws that govern the use of zip codes in rate-making. These laws typically require insurers to file their rates with the state insurance department for review and approval. The department may consider factors such as the risk profile of the area, the availability of competing insurers, and the impact on consumers.

Effectiveness of Regulations

The effectiveness of these regulations in ensuring fairness and transparency in insurance rates is a subject of ongoing debate. Some argue that regulations have been successful in preventing insurers from charging excessive rates in high-risk areas. Others contend that regulations can lead to higher rates for consumers in low-risk areas, as insurers spread the risk across all policyholders.

Potential Areas for Improvement or Reform

Potential areas for improvement or reform in the regulation of insurance rates by zip code include:

- Greater Transparency:Enhancing transparency in the rate-making process can help consumers understand how their rates are determined and identify potential disparities.

- Risk-Based Rating:Exploring risk-based rating systems that more accurately reflect the individual risk profile of policyholders, rather than relying solely on zip code.

- Consumer Protections:Strengthening consumer protections against unfair or discriminatory practices, such as redlining or the use of outdated data in rate-making.

Future Trends

The future of insurance rates by zip code is uncertain, but there are a number of trends that could impact rates in the coming years.

One trend is the increasing use of technology and data analytics in the insurance industry. Insurers are using data to better understand the risks associated with different zip codes, and this information is being used to set rates. As insurers continue to collect and analyze more data, it is likely that rates will become more accurate and personalized.

Impact of Technology

- Improved risk assessment

- More accurate and personalized rates

- Increased use of telematics and other data-gathering devices

Changing Demographics

Another trend that could impact insurance rates by zip code is changing demographics. As the population ages, the number of people who need long-term care insurance is increasing. This could lead to higher rates for long-term care insurance in areas with a large elderly population.

- Increasing demand for long-term care insurance

- Higher rates in areas with a large elderly population

- Potential impact on other types of insurance, such as homeowners and auto insurance

Last Point

As the insurance landscape continues to evolve, staying informed about the role of zip codes in determining rates is crucial for consumers and industry professionals alike. By understanding the factors at play, we can navigate the complexities of insurance and make informed decisions that protect our financial well-being.

FAQ

How do zip codes affect insurance rates?

Zip codes serve as indicators of various factors that insurance companies consider when setting rates, such as crime rates, property values, and natural disaster risks.

Can I negotiate my insurance rates based on my zip code?

While zip code is a significant factor, insurance rates are also influenced by individual factors like driving history or claims history. Negotiating rates may be possible based on these factors.

Are there any regulations governing insurance rates by zip code?

Yes, some states have regulations in place to prevent excessive rate variations based solely on zip code. These regulations aim to ensure fairness and protect consumers from discrimination.