Cash in term life insurance while still alive – Cashing in on term life insurance while you’re still alive is a unique financial strategy that can provide you with access to funds without having to wait until you pass away. This strategy can be a great option for those who need money for unexpected expenses, retirement, or other financial goals.

In this article, we’ll explore the ins and outs of cashing in on term life insurance, including the benefits, drawbacks, and alternatives.

When you purchase a term life insurance policy, you agree to pay a monthly premium in exchange for a death benefit that will be paid to your beneficiaries upon your death. However, if you outlive the term of your policy, the policy will expire and you will not receive any payout.

Cashing in on your policy allows you to access the cash value of your policy while you’re still alive, but it will terminate your coverage.

Understanding Life Insurance Policies: Cash In Term Life Insurance While Still Alive

Life insurance provides financial protection for your loved ones in the event of your untimely demise. Among various life insurance options, term life insurance stands out as a popular choice, offering coverage for a specific period.

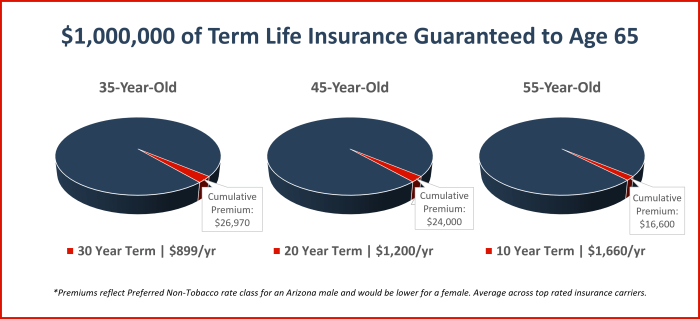

Term life insurance policies are designed to provide coverage for a predetermined period, such as 10, 20, or 30 years. During this period, the policyholder pays a fixed premium, and if they pass away within the coverage term, the beneficiaries receive the death benefit.

Benefits of Term Life Insurance, Cash in term life insurance while still alive

- Affordable:Term life insurance premiums are generally lower compared to other life insurance options, making it an accessible choice for individuals with limited budgets.

- Flexibility:Term life insurance policies offer flexibility in terms of coverage duration and premium payments, allowing policyholders to tailor the coverage to their specific needs.

- No Cash Value:Unlike whole life insurance, term life insurance policies do not accumulate cash value, which can be beneficial for individuals who prioritize pure death benefit protection.

Drawbacks of Term Life Insurance

- Limited Coverage Period:Term life insurance policies expire at the end of the coverage period, and if the policyholder outlives the term, they will no longer have coverage unless they renew or purchase a new policy.

- No Cash Value:As mentioned earlier, term life insurance policies do not build cash value, which means there is no financial benefit for outliving the coverage period.

Cashing In Life Insurance Policies

Cashing in a life insurance policy refers to surrendering the policy to the insurance company in exchange for its cash value. This action terminates the policy and the death benefit it provides.

Process of Cashing In a Life Insurance Policy

The process of cashing in a life insurance policy typically involves the following steps:

- Contact the insurance company and express your intent to surrender the policy.

- Provide the necessary documentation, such as the policy number and proof of identity.

- Receive a cash surrender value calculation from the insurance company.

- Review the calculation and decide whether to proceed with the surrender.

- Sign a surrender form and return it to the insurance company.

Advantages of Cashing In a Life Insurance Policy

There are several potential advantages to cashing in a life insurance policy:

- Access to cash:Cashing in a policy provides immediate access to a lump sum of money that can be used for various financial needs, such as paying off debt, funding education, or investing.

- Tax-free cash value:The cash value of a life insurance policy grows tax-deferred, meaning that withdrawals from the policy are not subject to income tax.

- Avoid policy lapse:If you can no longer afford the premiums on a life insurance policy, cashing it in can prevent the policy from lapsing and losing its value.

Disadvantages of Cashing In a Life Insurance Policy

However, there are also some potential disadvantages to consider:

- Loss of death benefit:Cashing in a life insurance policy means giving up the death benefit that it provides. This can leave your loved ones without financial protection in the event of your death.

- Surrender charges:Many life insurance policies impose surrender charges if the policy is cashed in within a certain period of time. These charges can reduce the amount of cash you receive.

- Missed growth potential:If you cash in a life insurance policy, you give up the potential for future growth in the policy’s cash value.

Ultimately, the decision of whether or not to cash in a life insurance policy is a personal one. It’s important to carefully consider the advantages and disadvantages before making a decision.

Alternatives to Cashing In

Cashing in a life insurance policy may not always be the best option. There are several alternatives that allow you to access funds from your policy without surrendering it.

When it comes to cashing in on a term life insurance policy while you’re still alive, it’s important to weigh your options carefully. You may want to consider reaching out to a reputable insurance provider like veronica meyers state farm insurance to get personalized advice.

They can help you explore different strategies for accessing the cash value of your policy while preserving your coverage.

The best alternative for you will depend on your individual circumstances and financial goals. It’s important to carefully consider all of your options before making a decision.

Policy Loans

Policy loans are a common way to access funds from a life insurance policy. They are secured loans that are backed by the cash value of your policy. This means that you do not have to provide any collateral, and the interest rates are typically lower than those on other types of loans.

However, policy loans do have some drawbacks. The interest on policy loans is not tax-deductible, and if you fail to repay the loan, your policy may lapse.

If you’re considering cashing in your term life insurance while you’re still alive, you may want to think about whether your boat insurance covers hurricane damage. Does boat insurance cover hurricane damage ? This is an important question to ask, as hurricanes can cause significant damage to boats.

If your boat is damaged in a hurricane, you’ll want to be sure that you have the coverage you need to repair or replace it.

Partial Withdrawals

Partial withdrawals allow you to take out a portion of the cash value of your policy without surrendering it. This can be a good option if you need a small amount of money and do not want to take out a policy loan.

However, partial withdrawals can also have some drawbacks. If you take out too much money, your policy may lapse. Additionally, partial withdrawals may reduce the death benefit of your policy.

Cashing in term life insurance while still alive can provide a lump sum of money for unexpected expenses or long-term goals. However, it’s important to consider the financial implications and consult with a financial advisor. If you’re also looking for reliable home insurance in Texas, check out best home insurance in texas reddit for comprehensive coverage and competitive rates.

Cashing in term life insurance can provide financial flexibility, but it’s crucial to make an informed decision based on your individual circumstances.

Accelerated Death Benefits

Accelerated death benefits allow you to receive a portion of the death benefit of your policy while you are still alive. This can be a good option if you are facing a terminal illness or other life-threatening condition.

However, accelerated death benefits can also have some drawbacks. The amount of money you can receive is limited, and your policy may lapse if you receive too much money.

Legal and Tax Implications

Cashing in a life insurance policy has legal and tax implications that should be considered before making a decision. It’s important to understand how these implications may affect you and your beneficiaries.

Impact on Beneficiaries

Cashing in a life insurance policy will terminate the policy and eliminate the death benefit for your beneficiaries. This could have a significant impact on their financial security if they were relying on the policy proceeds. It’s crucial to discuss your plans with your beneficiaries and consider their needs before making any decisions.

Tax Consequences

The proceeds from a life insurance policy are generally tax-free for beneficiaries. However, if you cash in the policy while you’re still alive, you may have to pay taxes on the gains. The amount of tax you owe will depend on the type of policy you have and how long you’ve had it.

Minimizing the Tax Burden

There are several strategies you can use to minimize the tax burden when cashing in a life insurance policy. One option is to take out a loan against the policy. This will allow you to access the funds without having to surrender the policy.

Cashing in term life insurance while still alive can be a way to access funds, but it’s important to consider the potential consequences. For example, if you cash out your policy, you’ll no longer have life insurance coverage. If you’re considering cashing out your policy, it’s a good idea to speak to a financial advisor to discuss your options.

Can you change insurance mid policy ? The answer is yes, but there are some things you should keep in mind. First, you’ll need to find a new insurance company that is willing to take you on as a client.

Second, you’ll need to pay a new application fee. Third, your new policy may have different terms and conditions than your old policy. Finally, you may have to wait a period of time before your new policy goes into effect.

Cashing in term life insurance while still alive can be a way to access funds, but it’s important to consider the potential consequences.

Another option is to exchange the policy for a new one with a lower death benefit. This will reduce the amount of taxable gains you’ll have to pay.It’s important to consult with a financial advisor or tax professional to determine the best strategy for your individual situation.

They can help you understand the legal and tax implications of cashing in a life insurance policy and make informed decisions about your financial future.

Ethical Considerations

Cashing in a life insurance policy involves significant ethical considerations that require careful evaluation. It’s essential to weigh the potential impact on family members and dependents before making a decision.

The primary ethical concern is the impact on beneficiaries. Life insurance policies are typically designed to provide financial security for loved ones in the event of the policyholder’s death. Cashing in the policy may deprive them of this vital financial support, especially if the policyholder is the primary income earner or has dependents who rely on the death benefit.

Beneficiaries’ Well-being

- Consider the financial needs and well-being of beneficiaries, especially if they are young, disabled, or have special needs.

- Assess the availability of alternative sources of income or financial support for beneficiaries.

- Evaluate the potential long-term consequences of depriving beneficiaries of the death benefit.

Another ethical consideration is the obligation to maintain the integrity of the insurance contract. Cashing in a policy may violate the trust established between the policyholder and the insurance company. It’s important to fulfill the agreed-upon terms and conditions of the policy, which typically include paying premiums and maintaining the policy in force until maturity.

Fiduciary Responsibility

- Recognize the fiduciary responsibility to beneficiaries, if applicable.

- Consider the potential legal implications of cashing in a policy, including breach of contract or fiduciary duty.

- Seek legal advice to ensure compliance with all relevant laws and regulations.

Ultimately, the decision of whether or not to cash in a life insurance policy is a personal one. It requires careful consideration of the ethical implications, potential impact on beneficiaries, and alignment with personal values.

Last Word

Ultimately, the decision of whether or not to cash in on your term life insurance policy is a personal one. There are both benefits and drawbacks to consider, and the best option for you will depend on your individual circumstances.

If you’re considering cashing in on your policy, it’s important to weigh the pros and cons carefully and to consult with a financial advisor to make sure you’re making the best decision for your financial future.

FAQ Overview

What are the benefits of cashing in on term life insurance?

There are several benefits to cashing in on term life insurance, including:

- Access to cash: Cashing in on your policy can provide you with a lump sum of cash that you can use for any purpose, such as paying off debt, funding a down payment on a house, or investing for retirement.

- Flexibility: Cashing in on your policy gives you the flexibility to access your funds whenever you need them, without having to wait until you pass away.

- Tax benefits: The cash value of your policy is not taxed until you withdraw it, so cashing in on your policy can be a tax-efficient way to access your funds.

What are the drawbacks of cashing in on term life insurance?

There are also some drawbacks to cashing in on term life insurance, including:

- Loss of coverage: Cashing in on your policy will terminate your coverage, so you will no longer have a death benefit in place to protect your loved ones.

- Surrender charges: Some policies have surrender charges that you will have to pay if you cash in on your policy before a certain period of time.

- Tax consequences: If you withdraw the cash value of your policy before you reach age 59½, you may have to pay income tax on the earnings.

What are some alternatives to cashing in on term life insurance?

There are several alternatives to cashing in on term life insurance, including:

- Policy loans: You can borrow against the cash value of your policy without having to cash it in. This can be a good option if you need to access funds quickly and you don’t want to terminate your coverage.

- Partial withdrawals: Some policies allow you to withdraw a portion of the cash value of your policy without having to cash it in. This can be a good option if you need to access a smaller amount of money.

- Viatical settlements: A viatical settlement is a transaction in which you sell your life insurance policy to a third party for a lump sum of cash. This can be a good option if you are terminally ill and you need to access funds quickly.