250 000 whole life insurance – 250,000 whole life insurance sets the stage for this enthralling narrative, offering readers a glimpse into a story that is rich in detail and brimming with originality from the outset. This comprehensive guide delves into the intricacies of whole life insurance, unraveling its key features, advantages, and considerations to help you make informed decisions about your financial future.

As we journey through this informative landscape, we will explore the nuances of whole life insurance, examining its guaranteed death benefit, cash value accumulation, and potential tax benefits. By shedding light on the factors that influence policy selection, including age, health, and financial goals, we empower you to choose a policy that aligns seamlessly with your unique circumstances.

Definition and Overview of Whole Life Insurance

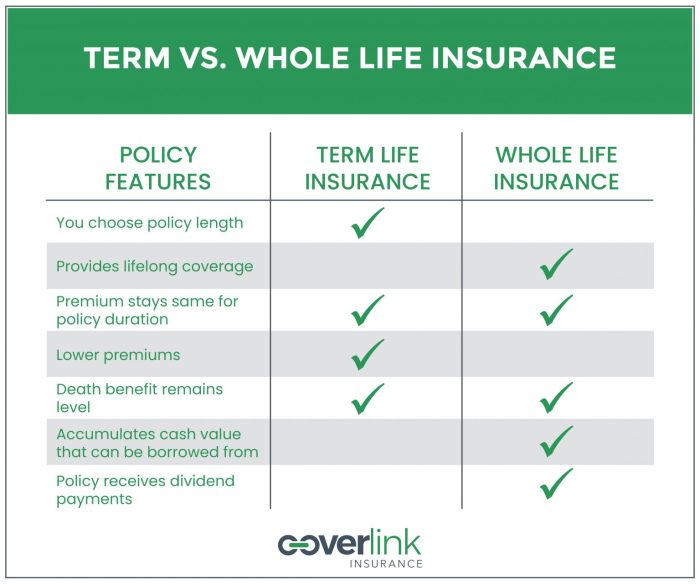

Whole life insurance is a type of permanent life insurance that provides coverage for your entire life, as long as you continue to pay the premiums. It also has a cash value component that grows over time, which you can borrow against or withdraw from.

Whole life insurance is more expensive than term life insurance, but it offers a number of benefits, including:

- Guaranteed coverage for your entire life

- A cash value component that grows over time

- The ability to borrow against or withdraw from the cash value

- Tax-deferred growth of the cash value

250,000 Whole Life Insurance

250,000 whole life insurance is a type of whole life insurance that provides $250,000 of coverage. This amount of coverage is typically sufficient to cover final expenses, such as funeral costs and outstanding debts. It can also be used to provide financial security for your family in the event of your death.

Benefits and Advantages of Whole Life Insurance

Whole life insurance offers numerous advantages, making it an attractive financial planning tool. These benefits include:

Guaranteed Death Benefit:Whole life insurance provides a guaranteed death benefit to your beneficiaries, ensuring they receive a specified amount of money upon your death. This financial cushion can help cover expenses like funeral costs, outstanding debts, or future living expenses, providing peace of mind to both you and your loved ones.

Cash Value Accumulation

Whole life insurance policies accumulate cash value over time, providing a potential source of funds for various needs. This cash value grows on a tax-deferred basis, meaning you can withdraw or borrow against it without incurring immediate taxes.

Potential Tax Benefits

Whole life insurance offers potential tax benefits. The death benefit is generally tax-free to your beneficiaries, and the cash value accumulation may also grow tax-deferred. This can be a significant advantage, especially if you anticipate being in a higher tax bracket in the future.

With a $250,000 whole life insurancepolicy, you can provide substantial financial security to your family. The guaranteed death benefit ensures they will receive a significant amount of money to cover expenses and maintain their standard of living. Additionally, the cash value accumulation can serve as a valuable savings tool for future financial goals or emergencies.

Factors to Consider When Choosing a Whole Life Insurance Policy

When selecting a whole life insurance policy, several key factors should be considered to ensure the policy aligns with your individual needs and financial goals. These factors include:

- Age:Age significantly impacts the cost of whole life insurance. Younger individuals typically pay lower premiums due to a lower risk of mortality.

- Health:Health status is a crucial factor in determining insurance premiums. Individuals with pre-existing medical conditions may face higher premiums or may be denied coverage altogether.

- Lifestyle:Certain lifestyle factors, such as smoking or engaging in hazardous activities, can increase insurance premiums due to an elevated risk profile.

- Financial Goals:The purpose and financial goals for purchasing whole life insurance should be carefully considered. Whether it’s for estate planning, providing financial security for loved ones, or supplementing retirement income, the policy should align with these goals.

Premium Costs

The factors discussed above directly influence the cost of whole life insurance premiums. Age, health, and lifestyle all contribute to the insurance company’s assessment of risk. Younger and healthier individuals with low-risk lifestyles generally qualify for lower premiums. Conversely, older individuals, those with pre-existing medical conditions, or those with high-risk lifestyles may face higher premiums.

Suitability

Determining the suitability of a $250,000 whole life insurance policy requires careful consideration of individual circumstances. For younger individuals with good health and long-term financial goals, such a policy may provide a solid foundation for financial security and estate planning.

However, for older individuals or those with health concerns, a smaller policy or a different type of insurance may be more appropriate.

Costs and Premiums of Whole Life Insurance

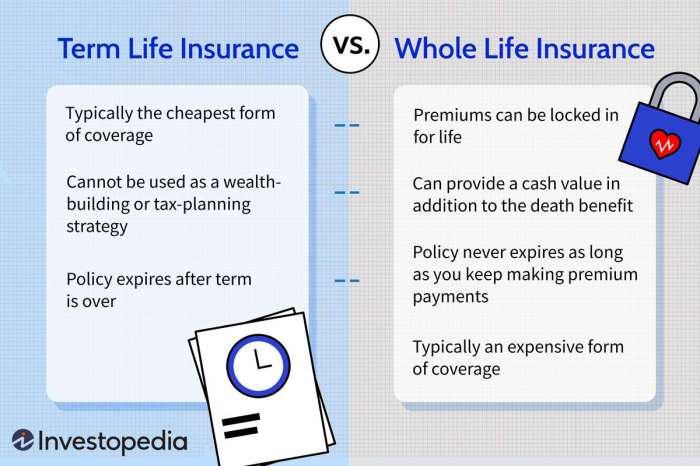

Whole life insurance premiums are typically higher than term life insurance premiums because whole life insurance provides lifelong coverage and a cash value component. The cost of whole life insurance depends on several factors, including your age, health, and the amount of coverage you need.

In addition to premiums, you may also have to pay policy fees and surrender charges. Policy fees are typically charged when you purchase a policy or make changes to your policy. Surrender charges are charged if you cancel your policy before it matures.

The amount of the surrender charge will depend on the length of time you have had the policy and the amount of cash value you have accumulated.

Premium Comparison

The premiums for a $250,000 whole life insurance policy will vary depending on the insurance company you choose and your individual circumstances. However, you can expect to pay more for a whole life insurance policy than you would for a term life insurance policy of the same amount.

For example, a 30-year-old male in good health can expect to pay around $30 per month for a $250,000 term life insurance policy. The same person would pay around $60 per month for a $250,000 whole life insurance policy.

Cash Value Accumulation and Growth

Whole life insurance policies accumulate cash value over time, which is a key feature that sets them apart from other types of life insurance. The cash value is a savings component that grows tax-deferred, meaning that you do not have to pay taxes on the earnings until you withdraw them.

The cash value of a whole life insurance policy can be used for a variety of purposes, such as:

- Supplementing your retirement income

- Funding a child’s education

- Purchasing a home

- Covering unexpected expenses

How Cash Value Accumulation Works

The cash value of a whole life insurance policy grows over time in two ways:

- Premiums:A portion of each premium you pay goes towards the cash value.

- Interest:The cash value earns interest at a rate set by the insurance company.

The cash value of a whole life insurance policy is not guaranteed, but it is typically credited at a rate of 2-4% per year. Over time, this can add up to a significant amount of money.

Example

Let’s say you purchase a $250,000 whole life insurance policy at the age of 30. You pay an annual premium of $1,000. After 20 years, the cash value of your policy could be around $25,000.

This cash value could be used to supplement your retirement income, fund a child’s education, or purchase a home. You could also withdraw the cash value tax-free, although this would reduce the death benefit of your policy.

Riders and Additional Benefits

Whole life insurance policies can be customized to meet specific needs and goals through the addition of riders and additional benefits. These optional add-ons provide extra coverage and protection, enhancing the value and functionality of the policy.

Accidental Death Benefit

An accidental death benefit provides an additional payout in the event of the policyholder’s accidental death. This benefit typically pays out a lump sum, which can be used to cover expenses such as funeral costs, outstanding debts, or lost income.

Disability Income Rider

A disability income rider provides a monthly income stream if the policyholder becomes disabled and unable to work. This benefit can help offset lost wages and provide financial stability during a period of disability.

Long-Term Care Coverage

Long-term care coverage provides financial assistance for expenses related to long-term care, such as nursing home care, assisted living, or home health care. This benefit can help ensure that the policyholder has access to the care they need without depleting their assets.

Comparison with Other Financial Products: 250 000 Whole Life Insurance

Whole life insurance differs from other financial products in terms of its features, benefits, and suitability for specific financial goals.

Term Life Insurance

- Pros:Lower premiums, provides temporary coverage for a specified period.

- Cons:No cash value accumulation, coverage expires after the term ends.

Annuities

- Pros:Provides guaranteed income stream during retirement, tax-deferred growth.

- Cons:Limited flexibility, surrender charges, and may not provide sufficient coverage for unexpected events.

Retirement Savings Plans, 250 000 whole life insurance

- Pros:Tax-advantaged growth, potential for higher returns, and flexibility in withdrawals.

- Cons:No death benefit, subject to market fluctuations, and may require regular contributions.

“250,000 whole life insurance” fits into a comprehensive financial strategy as it offers a combination of life insurance protection, cash value accumulation, and potential death benefit. It is suitable for individuals seeking long-term coverage, cash value growth, and a tax-advantaged savings vehicle.

End of Discussion

In the tapestry of financial products, whole life insurance stands out as a versatile and enduring choice. By providing a comprehensive overview of its benefits, costs, and riders, this guide has equipped you with the knowledge to make a well-informed decision about whether 250,000 whole life insurance is the right choice for you.

Remember, financial planning is an ongoing journey, and we encourage you to consult with a qualified professional to tailor a strategy that meets your specific needs and aspirations.

FAQ Summary

What is the key difference between whole life insurance and term life insurance?

Whole life insurance provides lifelong coverage and accumulates cash value over time, while term life insurance offers temporary coverage for a specific period.

How does the cash value accumulation in whole life insurance work?

A portion of your premiums goes towards building cash value, which grows at a set interest rate and can be borrowed against or withdrawn.

What are the advantages of adding riders to a whole life insurance policy?

Riders can enhance your coverage by providing additional benefits, such as accidental death benefits, disability income, and long-term care coverage.

How do I determine the right amount of whole life insurance coverage for me?

Consider your income, expenses, debts, and financial goals to estimate the amount of coverage you need to provide financial security for your loved ones.