100 000 life insurance cost – 100,000 life insurance cost: A topic that deserves attention. We’ll explore the factors that affect premiums, the different coverage options, how to compare providers, and tips for getting the best value. Get ready to navigate the world of life insurance like a pro!

As we dive into the details, remember that every individual’s situation is unique. The cost of 100,000 life insurance will vary depending on your age, health, lifestyle, and other factors. But by understanding the key concepts, you can make informed decisions and secure the coverage you need at a price you can afford.

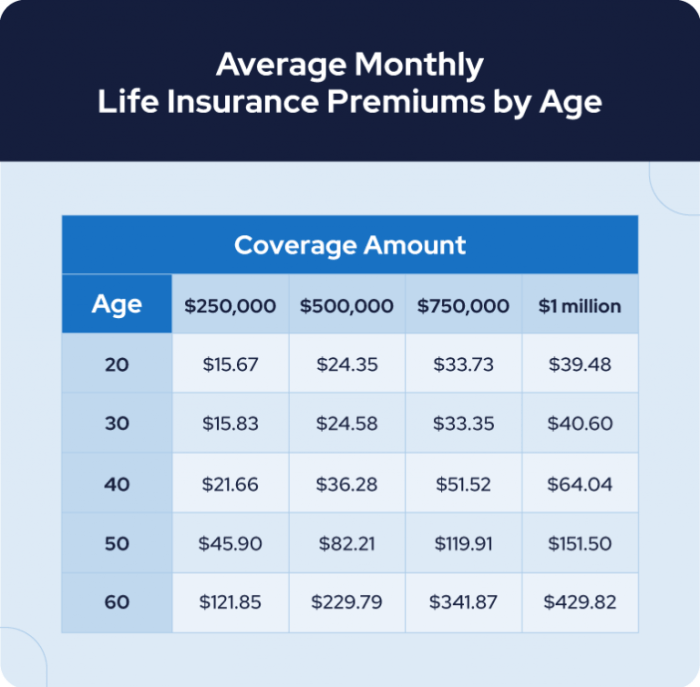

Factors Affecting Cost of Life Insurance

The cost of life insurance is determined by several factors, including your age, health, lifestyle, occupation, and hobbies. Here’s a breakdown of how each of these factors can impact your premiums:

Age

As you get older, your risk of dying increases, which means your life insurance premiums will be higher. This is because insurance companies have to pay out more claims for older people than for younger people.

Health and Lifestyle

Your health and lifestyle also play a role in determining your life insurance premiums. If you have a chronic health condition, such as heart disease or cancer, your premiums will be higher. This is because you are more likely to die from these conditions than someone who is healthy.

Your lifestyle choices can also affect your premiums. If you smoke, drink alcohol excessively, or are overweight, your premiums will be higher. This is because these behaviors increase your risk of dying.

Occupation and Hobbies, 100 000 life insurance cost

Your occupation and hobbies can also influence your life insurance premiums. If you have a dangerous occupation, such as a firefighter or police officer, your premiums will be higher. This is because you are more likely to die on the job than someone who has a less dangerous occupation.

Your hobbies can also affect your premiums. If you participate in high-risk activities, such as skydiving or rock climbing, your premiums will be higher. This is because you are more likely to die from these activities than someone who does not participate in these activities.

Coverage Options and Premiums: 100 000 Life Insurance Cost

Life insurance policies come in various coverage options and premium structures. Understanding these factors is crucial for selecting the right policy that aligns with your financial needs and risk tolerance.

Coverage Amount

The coverage amount is the death benefit that will be paid to your beneficiaries upon your demise. It determines the premium you pay and the level of financial protection you provide to your loved ones. Generally, higher coverage amounts result in higher premiums.

Term Life Insurance

- Provides coverage for a specific period, such as 10, 20, or 30 years.

- Premiums are typically lower compared to permanent life insurance.

- If you pass away during the coverage period, the death benefit is paid to your beneficiaries.

- No cash value accumulation or investment component.

Permanent Life Insurance

- Provides lifelong coverage as long as premiums are paid.

- Premiums are generally higher than term life insurance.

- Builds cash value over time, which can be borrowed against or withdrawn.

- Can be used as a financial planning tool for retirement or wealth accumulation.

Riders and Additional Benefits

Riders are optional add-ons that can enhance your life insurance coverage. They typically come with an additional premium cost. Common riders include:

- Waiver of premium rider: Waives premium payments if you become disabled.

- Accidental death benefit rider: Provides an additional death benefit in case of accidental death.

- Long-term care rider: Provides coverage for long-term care expenses.

Comparing Insurance Providers

When evaluating life insurance policies, it’s crucial to compare quotes from multiple providers to secure the best coverage at the most competitive premium. This process involves not only comparing premiums but also carefully scrutinizing the coverage details to ensure they align with your specific needs and circumstances.

Factors to Consider When Comparing Providers

- Financial Strength:Assess the provider’s financial stability through independent ratings agencies like AM Best, Standard & Poor’s, and Moody’s.

- Customer Service:Consider the provider’s reputation for prompt and responsive customer support, as you may need assistance with policy changes, claims, or inquiries.

- Policy Flexibility:Evaluate the provider’s options for customization, such as riders, coverage amounts, and premium payment schedules, to ensure they meet your changing needs.

- Underwriting Process:Understand the provider’s underwriting guidelines and medical requirements, as these can impact the availability and cost of coverage.

- Reputation and Reviews:Research the provider’s industry reputation and customer reviews to gauge their overall reliability and satisfaction ratings.

Getting the Best Value

Securing the most favorable deal on life insurance requires strategic planning. By understanding the factors that influence premiums and adopting savvy negotiation techniques, you can maximize your coverage while minimizing costs.

To qualify for lower premiums, consider the following tips:

- Maintain a healthy lifestyle:Engage in regular exercise, maintain a balanced diet, and refrain from smoking. These habits contribute to overall well-being and reduce the likelihood of health complications that could impact your premiums.

- Obtain a higher education:Individuals with advanced degrees typically have lower mortality rates and are viewed as lower risks by insurance companies.

- Choose the right coverage amount:Avoid over- or under-insuring yourself. Determine the appropriate coverage amount based on your financial obligations, dependents, and future goals.

- Consider a term life insurance policy:Term life insurance provides coverage for a specific period, typically 10, 20, or 30 years. This option is generally more affordable than whole life insurance, which provides coverage for your entire life.

Shopping around for insurance is crucial to secure the best value. Compare quotes from multiple providers to assess the most competitive rates and coverage options. Utilize online insurance marketplaces or consult with an independent insurance agent to streamline the comparison process.

Negotiating with insurance companies can also yield positive results. Be prepared to discuss your health history, lifestyle, and financial situation. Explain your rationale for seeking a lower premium and provide evidence to support your request. By presenting yourself as a responsible and low-risk applicant, you may be able to negotiate a more favorable rate.

Summary

Understanding the 100,000 life insurance cost is crucial for making informed financial decisions. By considering the factors that influence premiums, comparing coverage options, and negotiating with insurance companies, you can secure the protection you need without breaking the bank. Remember, life insurance is not just about protecting your loved ones financially; it’s about giving them peace of mind knowing that their future is secure.

Popular Questions

How does age affect life insurance premiums?

As you age, the risk of health issues increases, which can lead to higher premiums.

What role do health and lifestyle factors play in determining life insurance costs?

Smokers, individuals with chronic health conditions, and those who engage in risky activities may pay higher premiums.

Can my occupation or hobbies influence my life insurance premiums?

Yes, certain occupations and hobbies that involve high levels of risk may result in higher premiums.